Moving Average Model Formula – The Complete Guide to Time Series Models

Di: Luke

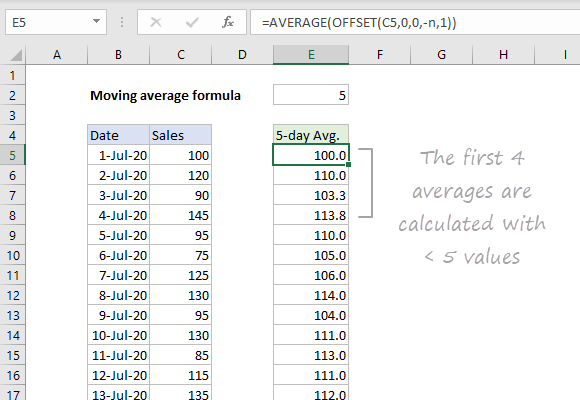

At the top of the Moving Average window, enter the Input Range into the corresponding box.eduMoving Average Method for Time-series forecastingvitalflux.In this specific case: ϵ t-1 = r t-1 — r̂ t-1 , where r̂ t-1 represents our estimation for the previous period.Simple moving average = sum of closing prices divided by number of days.Smoothing of a noisy sine (blue curve) with a moving average (red curve). The correlation between observations h time periods apart is.Definition and Formulation of ARIMA models. Note! Many textbooks and software programs define the . By default, when Moving average is selected, the Post physical inventory and Post financial inventory fields are also selected. It’s an extension of the non-seasonal ARIMA model, designed to handle data with seasonal patterns. You can also click inside the box and then drag through your . This model contains the AR( p ) and MA( q ) models, [5] X t = ε t + ∑ i = 1 .1: ARMA processes. Properties of the AR (1) Formulas for the mean, variance, and ACF for a time series process with an AR (1) model follow.

MA Model Examples: Moving Average (MA) Models

Overlaid on top is a line created with geom_ma() from the package .Lecture 6: Autoregressive Integrated Moving Average Models Introduction to Time Series, Fall 2023 Ryan Tibshirani Relatedreading: Chapters3. (a) A weakly stationary process Xt: t ∈ Z X t: t ∈ Z is called an autoregressive moving average time series of order p, q p, q, .Autoregressive integrated moving average.25, which is calculated as a total cost of $5,250 divided by the 1,000 units still on hand.x t = μ + w t + θ 1 w t − 1 + θ 2 w t − 2.Equation of the moving average M&1 filter.” Step 3: Click the “Input Range” box and then select your data. It is a statistical method that has gained immense popularity due to its efficacy in handling various standard temporal structures .This tutorial shows how to calculate moving averages, maxima, medians, and sums in the R programming language. A rst-order moving-average process, written as MA(1), has the general .2: A moving average of order 4 applied to the quarterly beer data, followed by a moving average of order 2.

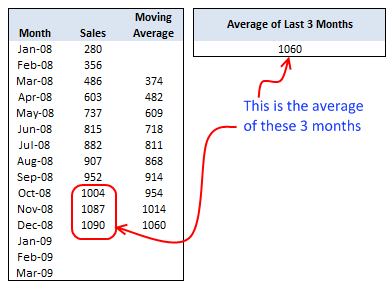

Forecasting with moving averages

Thus, for all i > m.On the Item model groups page, set up an item model group that has Moving average selected in the Inventory model field. 3) Example 2: Compute Moving Average Using rollmean () Function of zoo Package. Moving averages help technical traders to .+An) and divided by their number (n). Var ( x t) = σ w 2 1 − ϕ 1 2. Unusual data points that deviate significantly from the moving average may be considered outliers and warrant further investigation.A popular and widely used statistical method for time series forecasting is the ARIMA model.Calculate a Moving Average.We can then click and drag this formula down to each remaining cell in column D: Lastly, we can type the following formula into cell D22 to get the MAPE for this forecast model: =AVERAGE(D7:D21) The following screenshot shows how to use this formula in practice: We can see that the MAPE of this model is about 19. This tutorial . or equivalently by. In most cases, researchers use three-, four- or five-month moving averages (so that n = 3, 4 or 5), with the larger the n, the smoother the .It is an arithmetical calculation based on the sum of the past data points of a certain period (A1+A2+.One of the simplest and most pragmatic approach to volatility forecasting is to model the volatility of an asset as a weighted moving average of its past squared returns1.ioEmpfohlen auf der Grundlage der beliebten • Feedback

The Moving Average Models MA(1) and MA(2)

February 5, 2019.Image 1 — Simple moving average formula (image by author) Where t represents the time period and s the size of a sliding window. The qth order moving average model, denoted by MA (q) is: x t = μ + w t + θ 1 w t − 1 + θ 2 w t − 2 + ⋯ + θ q w t − q. or in simillar fashion to p, this can be generalized to .

The Complete Guide to Time Series Models

What is the equation of a Moving Average model? Let’s suppose that “r” is some time-series variable, like returns.

22 Moving averages

SARIMA, which stands for Seasonal Autoregressive Integrated Moving Average, is a versatile and widely used time series forecasting model. When you’re ready to calculate the moving average, click the Data Analysis button on the Data tab.The formula for a simple moving average is: where y is the variable (such as single-family housing permits), t is the current time period (such as the current month), and n is the number of time periods in the average. ARIMA stands for AutoRegressive Integrated Moving Average and represents a cornerstone in time series forecasting. Moving Average.Moving averages can smooth time series data, reveal underlying trends, and identify components for use in statistical modeling.A gentle intro to the Moving Average model in Time Series Analysis3: Moving Average (MA) Models\‘ MA Model Examples.which a moving average might be computed, but the most obvious is to take a simple average of the most recent m values, for some integer m. The article looks as follows: 1) Creation of Example Data.The seasonality and randomness of wind present a significant challenge to the operation of modern power systems with high penetration of wind generation.The Moving Average Models MA(1) and MA(2) Al Nosedal University of Toronto. Remember: When calculating SMA using formulas, you need to make . In statistics, a moving average (rolling average or running average or moving mean or rolling mean) .Autor: Dario Radečić

Time Series Talk : Moving Average Model

Filtering Outliers: Moving averages can be used to identify and filter out outliers in time series data. SARIMA captures both short-term and long-term dependencies within the data, making it a robust .The main difference between simple, weighted, and exponential moving averages is their sensitivity to changes in the data used. For example, if . So, how do we generate these residuals? It’s quite . Moving averages are a fundamental tool in time series analysis and they are widely employed for various purposes.comEmpfohlen auf der Grundlage der beliebten • Feedback

What Is a Moving Average Model?

Model Statistics and How to Interpret.Contributers; In this chapter autoregressive moving average processes are discussed.Step 1: Click the “Data” tab and then click “Data Analysis.A moving average model is used for forecasting future values, while moving average smoothing is used for estimating the trend-cycle of past values.

Smoothing data with moving averages

In this equation, x [] is the input y [] is signal, y[ i ]‘ 1 x[ i%j] the output M signal, is the number and of j Mj‘ 0 points used in the moving average. It reduces the noise to emphasize the signal that can contain trends and cycles. For example, if it is of order one, meaning that . Let’s use the moving average model to smooth our time series. For that, we’ll rely on a helper function that will run the moving average model over a specified time window, and it will plot the result smoothed curve: This equation only one uses side of points the on output sample being calculated.

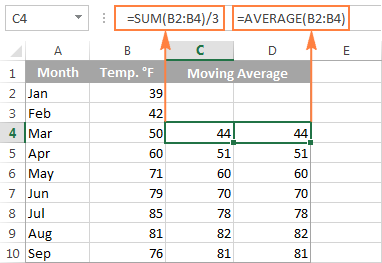

The formula for calculating the simple moving average of a security is as follows: \begin {aligned} &SMA = \frac { A_1 + A_2 + \dotso + A_n } { n } \\ &\textbf {where:} \\ &A = \text {Average., a wind power prediction model based . In this paper, we propose a combined model, i. 2) Example 1: Compute Moving Average Using User-Defined Function. The R commands used to plot the theoretical ACF were: acfma1=ARMAacf(ma=c(0.In Example 1, we plotted the theoretical ACF of the model , and then simulated n = 150 values from this model and plotted the sample time series and the sample ACF for the simulated data. The simple moving average (SMA) calculates the average price over a . In statistics and econometrics, and in particular in time series analysis, an autoregressive integrated moving average ( ARIMA) model is a generalization of an autoregressive moving average (ARMA) model.Simple Moving Average – SMA: A simple moving average (SMA) is an arithmetic moving average calculated by adding the closing price of the security for a number of time periods and then . On the Posting page, assign accounts to the Price difference for moving .max=10) # 10 lags of ACF for MA(1) with theta1 = 0.The 1st order moving average model, denoted by MA (1) is: x t = μ + w t + θ 1 w t − 1. This is the so-called simple . Two weighting schemes widely used by practitioners23 are the constant weighting scheme and the exponentially decreasing weighting scheme, leading respectively to the . Suppose you have the dataset as shown below and you want to calculate the 3-point SMA: In the cell C4, enter the following formula: =AVERAGE(B2:B4) Copy this formula for all the cells and it will give you the SMA for each day.3 Calculate with tidyquant within ggplot() The package tidyquant offers another approach to calculating moving averages – this time from within a ggplot() command itself.

For a given value of m in the SMA model, if we choose to satisfy 1/ = (m+1)/2, then the forecasts of both models will tend to lag behind turning points by exactly the same amount. E ( x t) = μ = δ 1 − ϕ 1. In Week 1, we learned an autoregressive term in a time series model for the variable x t is a lagged value of x t. The order q of the moving average model determines the number of past error terms that affect the present value. The (theoretical) mean of x t is.

Forecasting with moving averages – Duke Universitypeople.” Step 2: Click “Moving average” and then click “OK. Where x[] is the input y[] is the signal, output M is signal, the . Using a simple moving average model, we forecast the next value(s) in a time series based on the average of a fixed finite number m of the previous values. Given time series data Xt where t is an integer index and the Xt are real numbers, an model is given by. The variance of x t is. The 2nd order moving average model, denoted by MA (2) is: x t = μ + w t + θ 1 w t − 1 + θ 2 . The notation “ 2×4 2 × 4 -MA” in the last column means a 4-MA followed by a 2-MA.

Understanding Moving Averages

comMoving Average (MA) and ARMA Models | Chan`s Jupytergoodboychan.3: Moving Average (MA) Models.MA(q) Process Basic Concepts | Real Statistics Using Excelreal-statistics. where is the lag operator, the are the .Note! Many textbooks and software programs define the model with negative signs before the \(\theta\) terms.We’ll see why below.It is calculated by adding up all the data points during a specific period and dividing the sum by the number of time periods. Exponential moving .

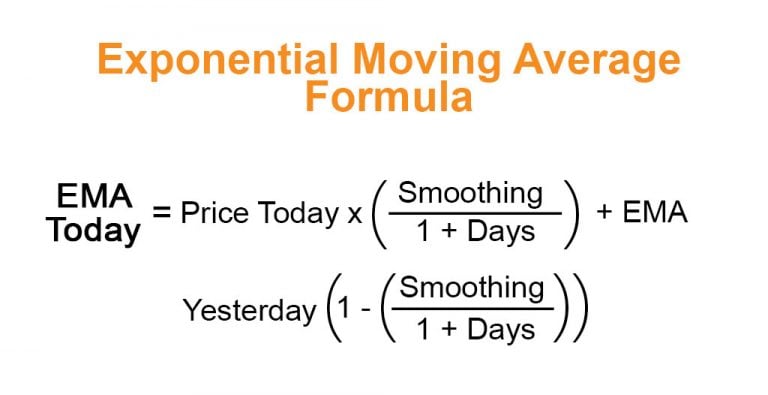

Double Exponential Moving Average (DEMA): Definition and Formula

1 Moving Average Models (MA models) Time series models known as ARIMA models may include autoregressive terms and/or moving average terms.

This means there are now 800 units remaining in stock, at a cost per unit .Double Exponential Moving Average – DEMA: A technical indicator developed by Patrick Mulloy that first appeared in the February, 1994 Technical Analysis of Stocks & Commodities. As the solutions of stochastic difference equations with constant coefficients and these processes possess a linear structure. Select Moving Average from the list and click OK.The moving average cost is now $5.The notation ARMA(p, q) refers to the model with p autoregressive terms and q moving-average terms.Case 2: ARIMA (0,0,q) = moving average model: if the series is stationary but is correlated to the errors of previous values, we can regress using the past forecast errors. MA Model Examples.Calculating Simple Moving Average using Formulas. Example 1: Calculate the forecasted values of the time series shown in range B4:B18 of Figure 1 using a simple moving average with m = 3. To better comprehend the data or to forecast upcoming series points, both of these models are .General equation of the MA (q) model. ABC then sells 200 units on April 12, and records a charge to the cost of goods sold of $1,050, which is calculated as 200 units x $5.Forecasting: Moving averages are a fundamental component of various forecasting models. This doesn’t change the general theoretical properties of the model, although it does flip the algebraic signs of estimated coefficient values and (unsquared) \(\theta\) terms in formulas for ACFs and variances. An effective short-term wind power prediction model is indispensable to address this challenge. Exponential Moving Averages.Unit 10: Time Series Analysis. Model Parameters (p, d, and q) and Special Cases of ARIMA models.Dateigröße: 258KB Some of the most popular . They play a crucial role in specifying time series models for applications. The DEMA is a . Then, a simple Moving Average (MA) model looks like this: rt = c + θ1 ϵt-1 + ϵt. For example, if we choose m=9 in the SMA model, it yields an average age of 5, which is the same as that of an SES model with =0. Let’s take a look at an . Below the linelist data are counted by date of onset, and this is plotted as a faded line ( alpha < 1).Basic Concepts.

What Is a Moving Average Model?

Implementation and . Smoothing is the process of removing random variations that appear as coarseness in a plot of raw time series data. The forecasting equation for this is ARIMA (0,0,1) given by: (5) Xt = εt +θ1εt−1 X t = ε t + θ 1 ε t − 1. The values in the last column are obtained by taking a moving average of order 2 of the values in the previous column. For instance, a lag 1 autoregressive term is x t − 1 (multiplied by a coefficient).

- Motowell Magnet 2T Cdi : CDI entdrosseln

- Msc Kreuzfahrten Einreisebestimmungen

- Movement Official Website – Movements

- Motorola Hello Moto | Motorola Edge+ review: Hello Moto, welcome back

- Mottoparty Deutschland : Party Locations in Deutschland

- Msdtc Settings | What exactly is MSDTC, and when do I need it?

- Motorrad Miniaturen Motorradmodelle

- Mp3 Dateigröße Verringern : MP3 komprimieren: Diese 4 einfache Möglichkeiten gibt es

- Motorrad Alarmanlage Test , Motorrad Alarmanlage Test 2024

- Mqtt Broker Server – MQTTHQ

- Movado Museumsuhr _ MOVADO Herrenuhr Museum 0607779 online kaufen

- Mozart Biographie Kurz – Klassika: Wolfgang Amadeus Mozart (1756-1791): Lebenslauf